With RFID contactless payment bank cards and travel cards like Oyster cards, accidental contactless payments can easily occur. Just by having your purse or wallet within range of a card terminal or access gate, there are also issues with multiple cards in proximity also known as “card clash”.

These types of convenient payment cards do not need the users to input or authorise the transaction with a pin. Users are unable to stop this happening without already having bought RFID protection or shielding (RFID shield wallet or RFID shield card).

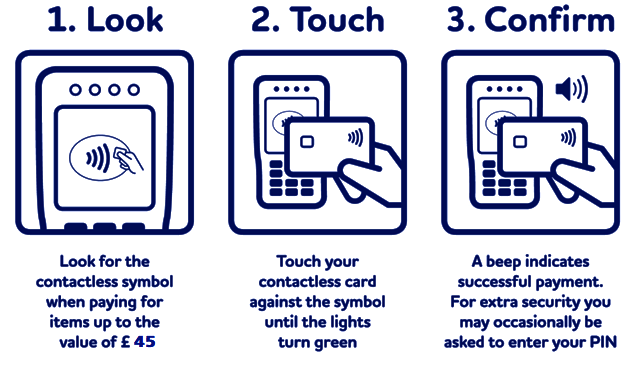

- Look, Touch, Confirm. It’s easy to use an RFID card and just as easy to make accidental RFID contactless payments

What you should do when an accidental RFID contactless payment happens

- Make a note of the date, time and location of the accidental contactless payment or transaction takes place. Keep any used tickets and receipts incase the service refuses to refund.

- Find your nearest member of staff or information point. Ask for information about disputing the contactless transaction error. Not all members of staff may know what to do, if this happens ask for complaints or a general enquiries telephone number and contact them.

- Are you using a travel service in London like the bus, Tube, tram, DLR, London Overground, TfL Rail, Emirates Air Line, River Bus and National Rail and have an online account? Login and check to see if you have been incorrectly charged. Note the transaction and register the dispute with Transport for London online. Or alternatively contact them by telephone 0343 222 1234 (call charges apply).

- If you are using Oyster travel card pay-as-you-go it is harder to prove ownership of the card when the transaction happened. So it is important you dispute the payment as soon as it happens with a member of staff.

- If you are unable to resolve the issue with the retailer or travel service, contact your bank with full details of the contactless payment and why you dispute the contactless payment giving full information. The bank can look into accidental payments on your behalf with the retailer/service.

How to prevent accidental contactless payments using RFID cards

- Most RFID contactless payment terminals work at short ranges. So keep your purse and wallets at least 20cm (8 inches) away from the terminal. Hacked or altered terminals and specialist readers can read up to 1.5m or further.

- Banks can send out VISA / MasterCards without contactless payment RFID chip included. Contact your bank and ask for one if you really do have concerns, but you will lose the convenience contactless payment brings.

- It is possible to render your bank card unable to use contactless payments by drilling through the chip inside the card. This is not recommended as you could damage the card so it is completely unusable, if you do this you will have to order another card from your bank and that could take time.

- A Faraday cage can block accidental contactless payments, and RFID payment cards. Conductive material such as aluminium foil, conductive paint, wire mesh, or any of a number of materials can block radio frequencies. Different materials are better and worse at blocking different frequencies. And the Faraday cage has to completely enclose the cards. So, no leaks or gaps, will mean no radio waves can get in or out, blocking the RFID signal. This method takes out the convenience out of contactless payment, it can work, but it’s not so easy to use.

- Purchase a good quality RFID blocking cards, wallets and purses. It must protect/shield 13.56 Mhz RF frequency. All RFID contactless payment cards use this international standard. If you have security cards or keyless passes these typically use RFID 125 khz. These are usually premium products and cost a bit more than a normal leather wallet or purse.

‘Do you want to learn more about contactless card protection? Read about this method of card protection.

How to get your money back

If you believe you have been a victim of contactless card fraud always, contact your bank immediately and to quote the Payment Services Regulations. These say that you must be refunded immediately if you are a victim of fraud.

If the bank can show that you were careless with your card and PIN or password, you will be liable for a maximum of £50, although many banks and building societies will waive this.

If that doesn’t work, then you can complain to the Financial Ombudsman.

Edited in June 2020